Putting digital at the heart of the economic recovery

COVID-19 has pushed digitalization everywhere. What’s needed now is the right government action to accelerate the transition to a smart economy.

Executive Summary

Digital technologies have played a crucial role in keeping society functioning during the COVID-19 pandemic, whether by enabling remote working, automating processes or facilitating contactless transactions. The increased use of digital technologies has also brought society closer to developing a smart economy, which promises new ways for businesses to grow and be more productive. We believe that governments need to accelerate these developments by placing digital at the core of the post-COVID-19 recovery, and propose an eight-point plan that sets out how digital technologies can be used to drive this recovery.

COVID-19: Part of a “perfect storm” bringing change

The past three decades have been characterized by rising global prosperity, with over 1 billion people lifting themselves out of extreme poverty, while a growing middle class has benefited from mass consumerism. Globalization and the internet revolution have created new business opportunities and improved productivity.

However, this positive trend has recently been upended by a perfect storm of threats to globalization, including rising economic uncertainty, increasing income inequality, and most recently, the COVID-19 pandemic.

COVID-19 in particular has rapidly impacted the way we live, do business, communicate with one another, learn and access information, feed ourselves, move around, and maintain our well-being.

Social distancing and other public-health measures introduced to combat the spread of COVID-19 have changed behaviors and brought scarcity of some goods and services. In several countries, entire populations have been under lockdown, with people required to stay home, shops and restaurants closed, public transportation suspended, and aircraft grounded. Our lives have continued, but much has changed.

Consumers and businesses alike have explored alternative ways of working and communicating, adopting new tools and methods they may not have considered before. Most notably, digital platforms have been used as a substitute for face-to-face interactions, often improving their efficiency.

As countries now begin to relax lockdown measures, the pace of recovery and adjustment to a “new normal” will differ by geography and industry. Different views of the future are emerging in the wake of COVID-19, including the technologies, business models and new behaviors it has introduced.

In this paper, we describe in Section 1 the impact and implications of COVID-19 for business; in Section II, we look at the role for digital in the new normal, identifying those industries that can benefit from digital transformation; and in Section III, we recommend what governments can do to encourage a sustained and rapid economic recovery.

1

COVID-19: Accelerating digital adoption and rethinking business models

The digital economy has benefited substantially from the COVID-19 crisis. Many of us now work remotely using cloud services and videoconferencing, consume entertainment from online subscription services (such as Netflix), order groceries and meals through digital platforms, and purchase a growing range of goods online. However, not all digital industries have benefited. Digital platforms that rely on human contact have suffered – for instance, ride hailing (e.g., Didi, Uber, Lyft) and property rental (e.g., Airbnb).

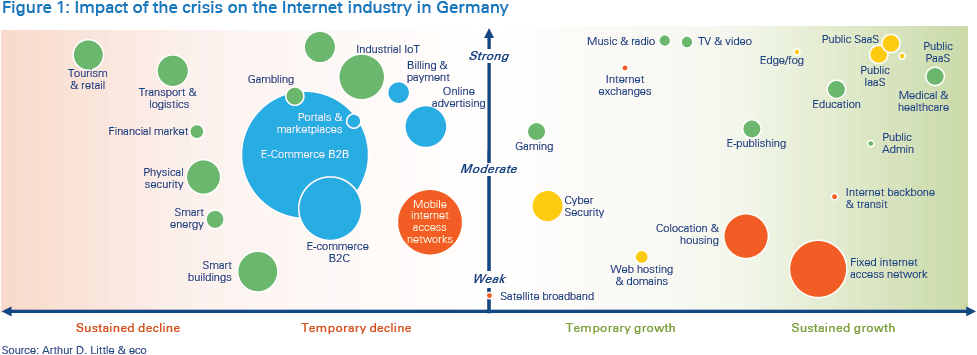

Figure 1 presents the impact of COVID-19 on the internet industry in Germany, based on research by Arthur D. Little for ECO, the German internet industry association. While there has been a pronounced shift in the share of B2B and B2C transactions carried out online, sales volumes declined as the economy shut down. A more nuanced analysis is therefore needed. Taking TV and video consumption as an example, Figure 1 shows that with many households in lockdown, consumption of TV has content increased. However, broadcasters have had to contend with plunging advertising revenues as the wider economy has contracted (not shown in the figure). Thus, the net impact on the industry may have been more negative than casual observation suggests. What COVID-19 has led to is a change in revenue share between traditional broadcasters and online streaming platforms. This move online to digital platforms has disrupted many sectors.

To better understand how COVID-19 is affecting different industry sectors, we have developed four categories of impact to evaluate the post-COVID-19 world:

- Rebound These are temporal changes which snap back to pre-crisis norms within relatively short periods. For example, apart from personal protective equipment being worn by employees, we would anticipate the demand for and provision of services such as hairdressing and taxi transport to change little post-COVID-19. Those familiar with the English pub might also expect crowds to return on match days to pre-COVID-19 levels. Equally, the availability of fresh foods at the grocer’s will likely return to normal as supply chains recover.

In a rebound, businesses seek short-term government support to survive until normal market conditions return. This support can include a deferral of business rates or tax relief. In the medium term, support is required to help businesses adapt to the new normal post-COVID-19. For example, investment in thermometry equipment to monitor and reassure both staff and customers, as these are safety measures that engender confidence, will support a rapid recovery. The “revenge consumption” seen in some countries as lockdown restrictions were lifted can be considered a severe rebound effect as consumer confidence returns.

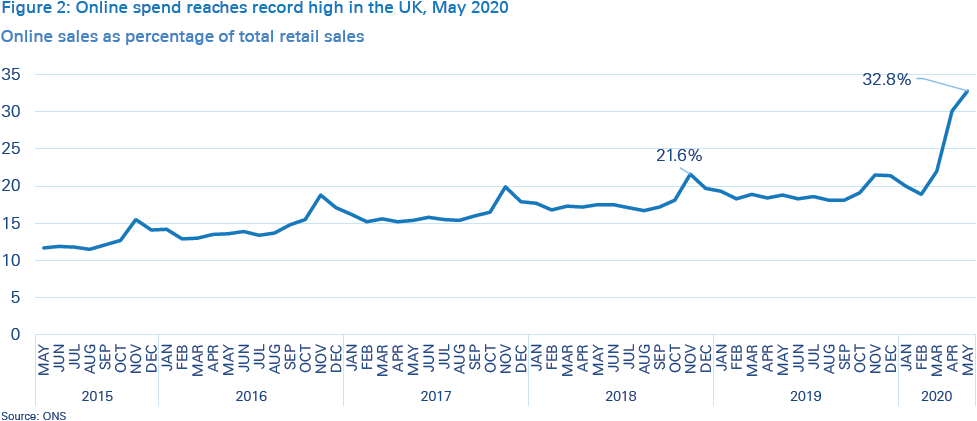

- Substitution This refers to permanent or semi-permanent changes in behavior and demand for goods and services. The crisis has seen many households adopt digital solutions for the first time – even the elderly, who are typically more reluctant to try new technologies, have been encouraged by home delivery and contactless interactions. For others, the move online has accelerated, as digitally savvy consumers have expanded their use of online platforms to purchase a wider range of perishables, consumer durables and entertainment. In short, COVID-19 has accelerated the adoption curve for many digital solutions – demand shifts which are unlikely to reverse. (See Figure 2 for the UK.)

The evolution of delivery platforms in China provides some examples of how retail businesses have adapted and are now flourishing despite the disruption. Meituan-Dianping and Alibaba’s Ele.me dominate the delivery-platform market in China. Although use of these platforms was already widespread before the crisis, due to their focus on food delivery, several developments have since given a boost to revenues:

- Platforms have introduced innovations such as contactless deliveries and prepared meals for home cooking, improving customers’ choice if they want to cook fresh and healthy meals at home, which is attractive to younger demographics

- Platforms’ expansion into delivering books, cosmetics and smartphones, partnering with the likes of Huawei and Sephora – a beauty-products chain – has leveraged the network effects of these platforms.

- New customers, specifically older and typically less digitally savvy groups, have been attracted to the platforms.

Restaurants devastated by loss of walk-in customers during lockdown have also been encouraged to join these platforms to deliver restaurant food to homes, changing their business models in the process. Even Michelin-starred restaurants in London and Hong Kong have made the move to food delivery.

Consolidating the move online for many businesses means using online sales platforms to digitalize backoffice operations for greater efficiency. By gathering procurement and sales data in real time, businesses can monitor inventories more accurately, automate purchasing and improve business planning. New services can also be offered as business use of digital platforms evolves and deepens – store pick-up, same-day delivery, advanced loyalty schemes based on customer analytics, personalized marketing, etc. Faced with substitution, businesses need to realign their strategies and operations with the new normal to optimize benefits. This may mean revising business plans and strategies to accommodate accelerated digital adoption and changing customer behavior or target segments. For smaller businesses, support will be required to upgrade IT equipment and skills in order to benefit from the digital economy. Moving online is the first necessary step for businesses to recover and thrive in the new normal.

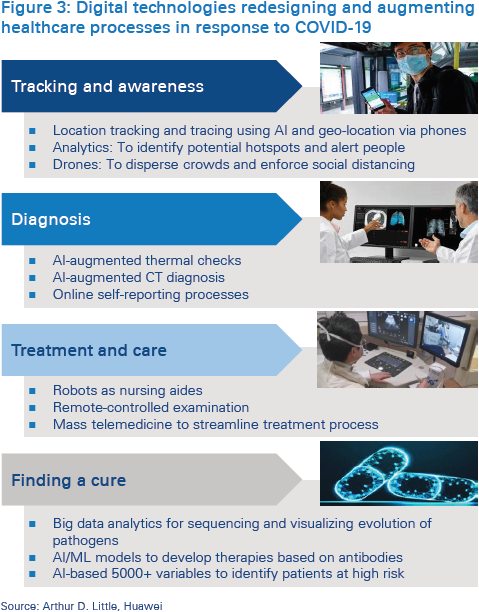

- Process This refers to changes in the ways of working and production incurred by COVID-19. New approaches have been developed during the crisis in response to social distancing and similar restrictions. Figure 3 illustrates how digital technologies have reinvented healthcare processes in response to COVID-19. The use of robots in hospitals to carry out repetitive tasks (such as cleaning and food delivery) has freed up valuable health-professional time for patient care. AI algorithms have enabled doctors to improve diagnosis reliability through augmentation. Manufacturing has been automated to protect workers. Drones have been used for last-mile delivery in logistics.

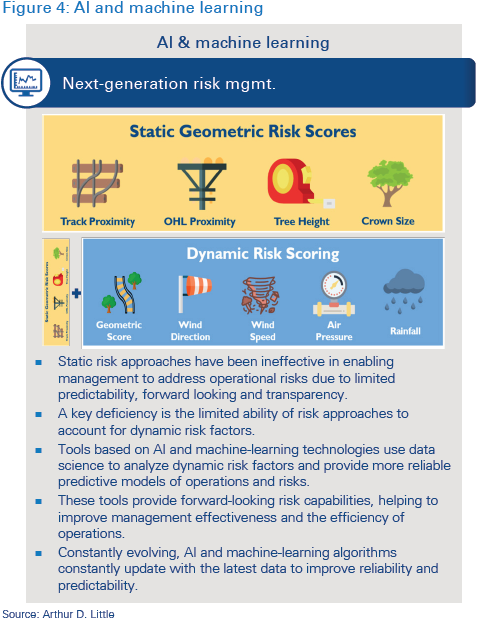

Digital tools enable businesses to redesign processes from the ground up, rebooting how work gets done and, in the process, redefining the business model to serve customers with improved products and greater efficiency. For example, in rail travel, this could mean automation of entire routes with driverless modules, which would allow capture of data at key junctures to manage passenger flows, provision of real-time journey information and insights to managers on asset condition and operational risks, and improvement of maintenance efficiency and reduction of downtime. Figure 4 provides a recent example of a rail operator using AI and machine learning to reinvent its risk management approach.

Home working is another process change that can be beneficial for employer and employee. A major telecoms player highlighted that its strong IT infrastructure had enabled its staff to work remotely and more flexibly during COVID-19 with no discernible impact on performance. Indeed, customers who normally had security concerns with different ways of working were much more accepting of new approaches and tools. A positive experience for both customer and supplier, experimentation has enabled this telecoms supplier to introduce more efficient processes.

With new technologies such as blockchain, the IoT and 5G communications currently being piloted in many industries and deployed at scale in others, we consider the current post-COVID-19 conditions conducive to further reinvention, rethinking of processes, investment and business planning.

- Revolution This defines cases in which both substitution and process changes occur in parallel. In other words, permanent or semi-permanent shifts in demand occur in tandem with process changes, which, in part, renders business models redundant. Industries are left to reinvent customer offerings and define more efficient processes and ways of working. Cruise tourism and passenger air travel are examples of sectors upended by the “perfect storm” of COVID-19 factors. In common with process changes, we foresee that these sectors will constantly evolve in the future to attract customers and improve operational efficiency. For example, augmented reality/virtual reality solutions will dispense with the need for many face-to-face interactions, leading to further reinvention.

Our prescription is to be bold. It is understandable that businesses may want to cut investment in a crisis and be more conservative in uncertain times, but bold decisions today can offer higher returns tomorrow. Moves such as rapid transformation from a restaurant to a delivery-based gourmet food-experience vendor, or migration of physical channels to online platforms (for banking and insurance processes), have saved businesses in the downturn and provided growth opportunities in the longer term. Bold businesses wishing to acquire new skills and digital capabilities through M&A will also find they can do so at lower cost in the downturn as valuations are depressed.

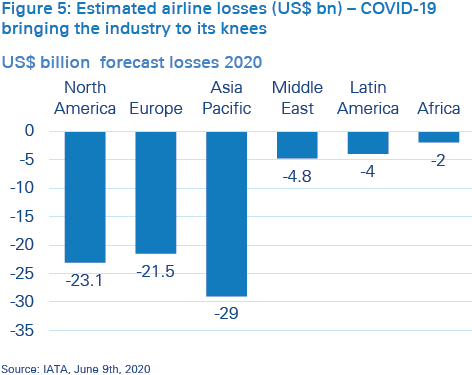

Due to the severity of disruption in “revolution” industries, government support is needed to make the bold yet necessary changes to create a sustainable future. For example, with airlines facing severe losses (see Figure 5 below), governments have provided cash injections to companies including Cathay Pacific, Lufthansa and Air France/KLM. The bold response is to use this cash to operate more fuel-efficient aircraft and reinvent service offerings around digital platforms, thus driving competitiveness, securing a sustainable future, and attracting customers back to air travel. Partnering with other stakeholders in the travel and transportation ecosystem is another bold initiative that could generate new efficiencies and create new service opportunities – for example, enhancing the door-to-door passenger experience.

Other challenges exist for airlines, such as protecting staff and passengers when onboarding and offboarding aircraft while maintaining social-distancing rules. Digital solutions to reduce human interaction can include app-based guidance and information for passengers, deployment of robots, and one-token travel identification. Predictive asset maintenance in operations and blockchain for the traceability of jet-engine parts in airline supply chains are further examples of where digital can reboot business models and help drive efficiency savings.

2

Digital in the new normal: Emergence of a smart economy

A smart digital economy

With rapid change and disruption continuing across many industries, the natural questions to ask are: where is this all leading? And how can businesses prepare and adapt for the future?

The changes we have described have a series of common features. They are:

- Autonomous through removing or limiting human interaction;

- Augmented to improve the effectiveness and efficiency of human actions;

- Highly agile and rapid in execution, and thus scalable;

- Digitally represented, enabling new insights to be gathered from data analytics;

- Interconnected and compatible, enabling devices to talk to and learn from each other.

These characteristics are consistent with what we consider to be a smart economy. The smart economy is enabled by multiple technologies with strong interdependencies. They include AI, machine learning, autonomous and assisted vehicles, edge computing, quantum computing, blockchain, big data analytics, and 5G telecommunications.

The end point in a smart economy is a fully connected and augmented world in which multiple devices talk and learn from each other to produce more efficient goods and services, which are personalized to the needs of the individual, with real-time functionality, and highly transactional. By being smart, industries improve productivity, create new opportunities for growth and generate higher returns. And by being able to pay higher wages, higher living standards and sustained economic prosperity are possible.

Indeed, for those economies and industries which have suffered weak productivity growth in recent years, a digital-led recovery from COVID-19 could be the step change needed to improve their long-term growth trajectory.

Digital as a driver of the economic recovery

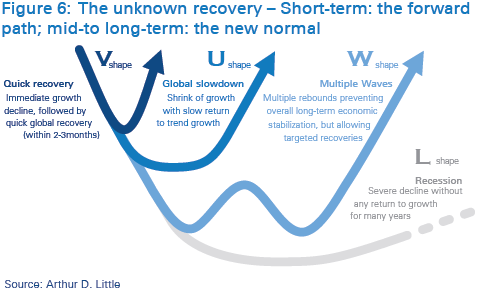

As we emerge from the COVID-19 global downturn, a rapid recovery is needed to prevent a spiral into prolonged economic depression. A V-shaped recovery (Figure 6) is now looking less likely as the pandemic is still ongoing in many parts of the world, with exports remaining depressed and supply chains disrupted. As such, the focus is now on a U-shaped recovery.

While digital technologies offer new ways for businesses to grow and be more productive, it is not completely clear how investments in new technologies impact productivity. A World Economic Forum study attempted to shed light on this issue based on data from over 16,000 companies in 14 industries, which was subject to econometric analysis of the productivity impacts.

It made four key findings in relation to companies’ returns on digital investments:

- The return on investment in new technologies is positive overall. The productivity increase is three times higher when technologies are deployed in combination – as would happen in a smart economy.

- The return on digital investments varies by industry, and industry leaders achieve greater productivity increases from investments in new technology than followers do (70 versus 30 percent), which reinforces the view that digitalization is a continuous process and organizations need to be agile.

- Asset-heavy industries realize more value from robotics; asset-light industries realize greater value from mobile/ social media, primarily led by efficiency-driven opportunities.

- While industry leaders have realized higher overall returns from robotics and mobile/social investments, followers have gained more from the IoT and cognitive technologies (artificial intelligence and big data analytics).

Although more research is needed to fully understand the impacts of digital investment by individual industry and economy, the findings clearly support the assumption that digital investment generates more than average positive returns. With COVID-19 accelerating digital adoption and forcing the reinvention of processes and business models, we believe that building on these advances is the best course of action to kickstart growth and avoid a protracted L-shaped recovery.

What does smart look like?

To reflect on what is already ongoing in many industry sectors, here are some case studies showing what a “smart” world may look like. The selected cases demonstrate how digital can have a transformative impact.

Smart hospitals improve patient care and operational efficiency using autonomous, augmented and AI technologies

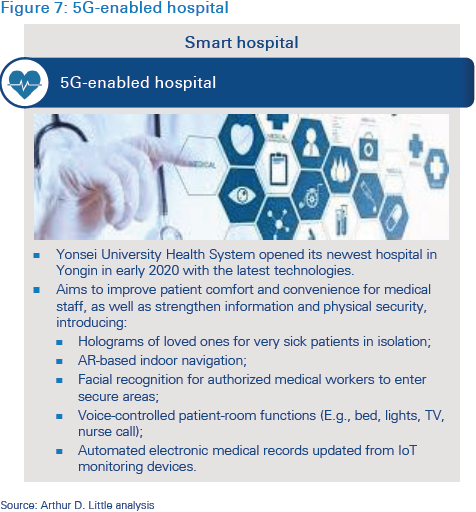

Aging demographics and rapidly rising costs are challenges facing public and private healthcare globally. The need to find new ways of working and efficiencies in healthcare delivery, while improving healthcare outcomes in treatment and prevention, are established priorities. Yongin hospital in South Korea was one of the first to introduce 5G, piloting several business use cases to improve patient comfort and generate operational efficiencies. (See Figure 7.)

We foresee healthcare being a leading beneficiary of digital technologies as the smart economy develops. Common features of future healthcare may include: telemedicine in pandemics to diagnose patients at safe distances, AI to aid doctors with diagnoses, patient monitoring via wearables, thermal imaging for body thermometry, chatbots for psychological consulting, and robots for logistics. The continual need to improve patient care and control healthcare costs makes it a fertile industry for the application of new digital technologies.

The airport of the future promises contactless, endto- end journeys and more efficient operations

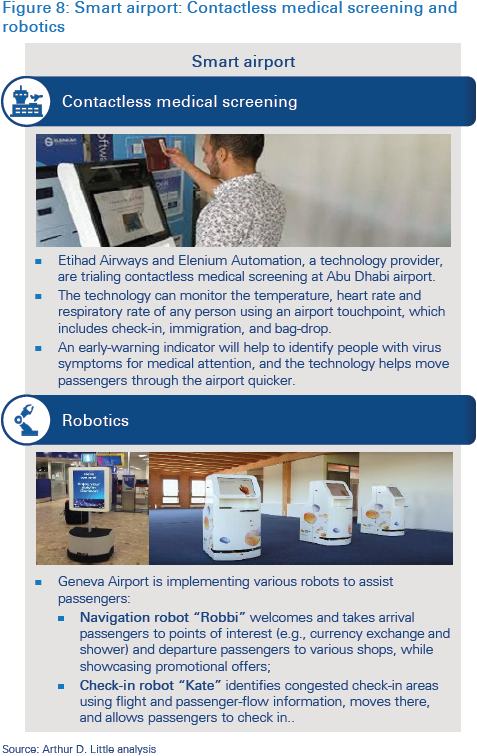

Applying digital technologies to airports can transform the end-to-end journey for passengers and generate efficiencies for operators. Post-COVID-19, there is a need to attract passengers back to air travel and re-establish profitable operations. Many airports have plans to go digital, and some are already in the process of implementing 5G, robotics and other technologies to improve customer experience and operational efficiency. We foresee that this transformation will now accelerate, with innovative solutions needed for testing passengers prior to airport arrival, limiting human contact during key touchpoints (check-in, customs, border control, boarding, etc.) and automating ground-handling operations. Figure 8 illustrates some of the technologies that Etihad Airways and Geneva Airport have already implemented to create a smart airport. Other examples reported in recent months include one-token identification at Tokyo Narita Airport planned for the 2021 Olympics, facial recognition at Beijing Airport, and autonomous vehicles at Hong Kong Airport.

The airport of the future will look very different to airports of today. With 5G deployment on the horizon and business use cases emerging, we anticipate that airports and other transporthub operators will increasingly emerge as digital leaders.

Traceability, real-time tracking and contactless are features of smart logistics

During COVID-19, a major challenge has been to introduce contactless last-mile delivery of medical goods and daily necessities to those with pre-existing medical conditions. Autonomous robots and drones were found to be an effective way of making these deliveries. A longer-term trend is the need to improve traceability and transparency in supply chains, for instance, to ensure the authenticity of pharmaceuticals or aircraft spare parts. For this, blockchain is being piloted to create immutable records in decentralized networks. Further examples of how these technologies are being used in logistics are provided in Figure 9, with more use cases certain to follow as supply chains become more complex and product origins need to be validated.

Smart energy grids are needed to connect new energy sources and safely manage energy supplies

Energy markets, specifically in Japan (as illustrated in Figure 10), some states in the US, and especially in Europe, are undergoing seismic changes that require digital solutions. To integrate renewable-energy sources with the power grid, manage supply and demand fluctuations, and enable the creation of the prosumer (households that sell surplus solar energy to energy suppliers on sunny days and consume energy on cloudy days), digital transformation is underway. Moving from centralized conventional generation technologies (coal, gas, nuclear) to decentralized renewable-energy sources (wind, solar, hydro) requires upgrading conventional grids to manage greater numbers of inputs and outputs, enabling real-time monitoring of energy consumption/production, and creating trading platforms for emission certificates.

We expect more regions to follow in the future, which will require 5G telecommunications, IoT devices, distributed ledger technologies and new business models to work in unison to manage energy suppliers and improve network resilience.

3 How to accelerate the economic recovery

We recommend an eight-point plan for governments to accelerate post-COVID-19 recovery via digital technologies:

1) Place digital at the core of the recovery strategy

Placing digital at the core of the recovery strategy and policy offers higher-than-average returns for the economy and society at large. This is why governments must include it in every single aspect of their recoveries, across initiatives and throughout all industries.

Aside from the economic benefits, going digital offers lifestyle and work changes that have positive impacts on the environment (fewer journeys and carbon emissions) and society (improved family life from working at home).

Fiscal stimulus packages with focus on digital include:

- South Korea A “Korean New Deal” aims to invigorate the convergence of new and old industries for greater job creation (see Figure 11), investing US$62 billion in establishing digital infrastructure, fostering industries that are online or do not require physical contact, and digitalizing infrastructure.

- European Union The European Commission is proposing to create a new recovery instrument: Next Generation EU – €750 billion of additional funding on top of an existing EU budget for 2021–2027 – a total of €1.85 trillion for a more sustainable, resilient and fairer Europe that places digital and green economic development at its core. (See “Push ‘green’ and digital together”, below.)

- Spain The central government is providing €16 billion to autonomous regions in support of two programmes: i) Giga society to encourage telecom operators to invest in better connectivity in low-yield areas; and ii) 5G pilot projects to fast-track deployment. The aim is to ensure all citizens and businesses (especially SMEs) can benefit from the digital economy.

The key levers for government are investment and regulation:

- Investment is needed to bring forward 5G deployment and next-generation access networks (NGA networks), and support business investment in digital transformation initiatives (training, ICT infrastructure, technology pilots, etc.). Investment is also required in digital cloud infrastructure (data centers), accompanied by regulation to determine where data is to be stored and computed, and under which regulatory framework

- Regulation should be used in parallel with investment. For example, placing obligations on telco operators (e.g., to connect rural/low-yield areas) and/or setting targets (e.g., for electric-vehicle deployment) can be powerful incentives for business and enablers of transformation.

More favorable regulation can also encourage private sector investment. Favorable regulation includes improved right-of-way access for infrastructure development, and rules that permit different business models and technologies to be applied in each market. Technology neutrality is critical if the best solutions are to be developed and find commercial value. In highly regulated sectors such as financial services and utilities, regulators should permit new products and business models, provided the risks created are adequately managed. Regulatory sandboxes are increasingly used to test new technologies in a controlled environment where the risks of a new business model or product can be assessed and understood. An example is the blockchain strategy of Germany’s federal government. Working with the tech industry, the regulator (BaFin) is defining the legal framework and supporting investment in this disruptive technology. As a result, Germany is becoming a blockchain leader.

2) Boost infrastructure investment

One of the core roles for governments is to provide infrastructure for its people and industries. This is even more critical for the digital economy: digital and ICT infrastructure must be a priority for governmental investment during the recovery, to lay the foundations of the smart economy. We would encourage public investment to go hand-in-hand with private investment in this area through public-private partnerships (PPPs).

High-quality fixed broadband should penetrate over 99 percent of households and businesses. Fiber and 5G rollout should be accelerated to give all businesses and households access to online opportunities in the digital economy. Regulators should also be encouraged to increase the spectrum available for 5G and LTE services, which can include short-term licenses or local licenses for campus/private networks. IT infrastructure investment is also required, particularly to enable SMEs to fully partake in the smart economy.

Many countries have now allocated 5G spectrum to operators, typically through auctions. However, to speed up the deployment of 5G, we recommend allocating more spectrum for unlicensed/shared usage. Large industrial sites, airports, sports stadiums and conference venues can make use of this additional spectrum to test and pilot new applications more quickly rather than wait for the widespread deployment of 5G. For example, we see smart-city initiatives in Hong Kong, Vienna, and Seoul deploying 5G in designated areas to accelerate use-case piloting and monetize the benefits.

Recognizing that 5G will help drive economic recovery and encourage business investment, New Zealand scrapped a planned 5G spectrum auction during COVID-19, implementing instead a fixed-price tariff to accelerate introduction. Japan adopted a similar policy, allocating 5G spectrum for free to operators, with obligations to invest in network development and coverage in exchange for licenses. The major benefit of these approaches is that operators have more capital left in the bank for infrastructure rollout. The opposite occurred in Italy, with auctions raising huge revenues for regulators, but leaving little on the balance sheets for deployment, which may now be delayed.

Arcep, the French regulator, has adopted a similar approach to Japan, requiring 25 percent of 3.4–3.8 GHz band sites in 5G deployment to be located in sparsely populated areas, thereby stimulating economic activity, notably manufacturing, and achieving high penetration and universal access, not just in metropolitan areas. Despite resistance among some operators and potential delays to 5G spectrum auctions, investment obligations are a better way of supporting a digital-driven recovery than via record-setting auctions.

3) Enable digital recovery for all, not just the happy few

The benefits of digitalization should be available to all. Inclusive access recognizes connectivity as a human right and an essential component in building a smart economy

A large digitalization gap exists between the world’s “haves” and “have nots”. For example, ADL research on SMEs (Figure 12) found that 87 percent of SMEs in Denmark had access to broadband speeds of at least 30 Mbps. In Columbia, this figure was 20 percent, and the sample average was 54 percent. The connectivity gap was equally wide between many urban and rural communities, with frequent media stories of homeworkers forced to walk up hills or visit coffee shops to access the connectivity necessary for videoconferencing or similar digital platforms.

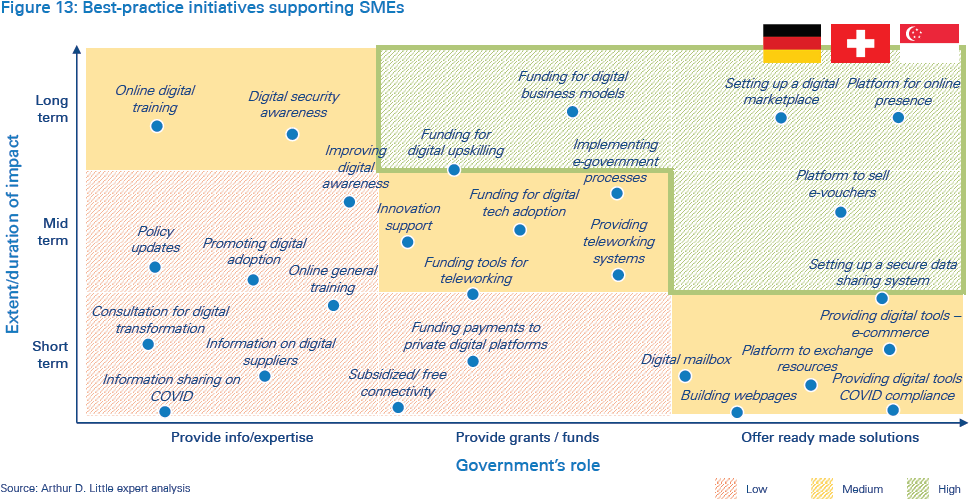

For SMEs, targeted government initiatives are needed to boost access for all businesses. Figure 13 identifies a number of targeted initiatives to support SMEs, including the provision of information to allow small businesses to make informed decisions, investment to enable digitalization, and ready-made solutions that businesses can adopt and/or participate in to boost revenues.

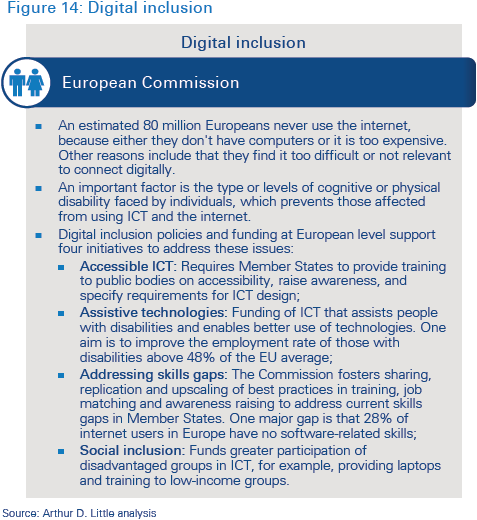

Access goes beyond SMEs and connectivity to also ensure that individuals have the necessary IT equipment and software. In some cases, this requires assistance for those who are most vulnerable in society. Recognizing that digital inequality is a major issue, the European Commission has introduced a digital inclusion policy supported by four initiatives to close the gap (Figure 14).

4) Double efforts to improve ICT skills and digital literacy

The effectiveness of digital investments in driving the economic recovery will depend to some extent on how businesses and individuals make use of digital solutions. Strong ICT skills and digital literacy are needed to optimize their use.

For some, this may involve learning how to use a tablet or online platform for the first time. For others, updating existing skills and developing new capabilities can create value and opportunity. For the more digitally savvy, upskilling more workers in programming and advanced technologies is needed to ensure businesses can recruit from a larger pool of capable workers. Indeed, a focus of South Korea’s New Deal is the training of new AI and software talents.

Among schoolchildren, measures implemented during COVID-19, such as free software licenses (Hong Kong) and laptops (UK), have been effective in boosting the number of students able to participate in lessons online and develop e-skills. For adults, Microsoft has offered six-month free subscriptions to its Teams software, which, in part, has accelerated the move to remote working for individuals and businesses.

In summary, a digital recovery for all should continue the initiatives introduced during COVID-19 to connect all households and businesses, as well as improve IT equipment access and skills.

5) Push “green” and digital together

As society becomes more environmentally conscious and aware of the need to address climate change, going digital should also mean going “green”. Virtual working and more efficient production go hand in hand with a cleaner environment and reduced resource depletion.

In launching the EU’s proposal for its next-generation stimulus package, European Commission president Ursula von der Leyen explicitly tied green outcomes to the recovery and digitalization, stating:

“The recovery plan turns the immense challenge we face into an opportunity, not only by supporting the recovery but also by investing in our future: the European Green Deal and digitalization will boost jobs and growth, the resilience of our societies and the health of our environment...”

The proposal provides additional stimulus funding via taxes on non-recycled plastics and carbon emissions, among other revenue sources. South Korea and Germany have also included environmental objectives in their post-COVID-19 stimulus plans. As these are export-led economies aiming to be leaders in electric vehicles, green energy infrastructure and autonomous technologies, a dual digital/green policy focus is a logical step to support industry competitiveness.

It is not just export economies that can benefit. For instance, Pakistan has also introduced a green COVID-19 stimulus package to improve energy efficiency and resilience in its construction sector.

6) Use the government as a catalyst for digital adoption

To drive broader digital transformation of the economy and reward innovation and reinvention, governments must do two things:

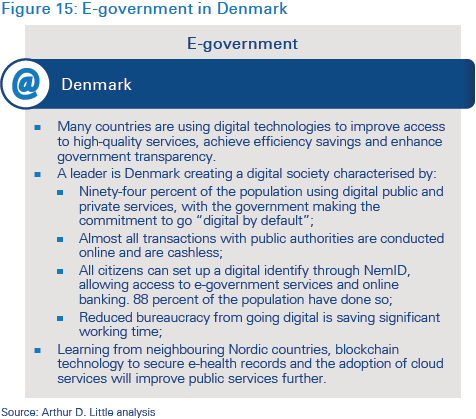

Firstly, government should embrace digital technologies to improve the quality and efficiency of public services. Denmark is a leader in this regard. (See Figure 15.) By becoming a digital leader itself, government demonstrates confidence in the technology, positively signalling its benefits, reliability and affordability to businesses and households. Early support can accelerate private sector adoption and encourage further innovation by establishing a market for innovators.

Secondly, government should leverage its position as a user and regulator of digital services to establish standards and remove regulatory obstacles to digital adoption. For example, asset tokenization and smart contracts based on blockchain technology are slow to penetrate markets. Establishing regulatory frameworks that provide legal certainty, develop standards for how data is managed, and specify minimum performance requirements can accelerate adoption and development.

Our recommendation is that governments should be bold, not just in investing in digital. Governments should use digital solutions and create the regulatory conditions conducive to innovation.

7) Empower small businesses and consumers

Empowering consumers and small businesses to adopt and use digital technologies is an important factor in accelerating the economic recovery. Consumers and businesses must have confidence in the reliability and security of digital solutions, but also have the information to hand to make informed purchasing and data-sharing decisions. A recent example is the reluctance of many to use COVID-19 tracing apps in some countries over concern for data security and privacy. Similar concerns exist for small businesses when sharing data in industry consortia or with suppliers.

Publishing use cases is an important first step in understanding the benefits of a technology and what additional risks it may generate. From a legal perspective, consumers want reassurance that a digital purchase is equivalent to making a physical purchase (i.e., the level of protection and rights are the same whether a download or physical product).

Measures are ongoing to strengthen security and protection for small businesses and consumers in the digital economy, with due consideration given to maintaining digital sovereignty. The European Union’s digital single market is one of the most prominent examples, and it is currently in the process of implementing laws to protect businesses and consumers online, which include:

- New rules to stop unjustified geo-blocking;

- Strengthening consumer rights when purchasing online and cross-border;

- New rules on digital contracts;

- New VAT rules for online sales of goods and services;

- New rules to remove sites or social media accounts where scams have been identified;

- A new legal framework that guarantees transparent terms and conditions for business users of online platforms.

Businesses and consumers are also concerned by data protection and cybersecurity issues. Global rules would help to ensure that data exchanged through online platforms is equally protected, regardless of where the platform owner or hosting servers are located. For cloud infrastructure, similar challenges exist. Establishing where data is stored and computed must occur before the regulatory framework can be agreed.

In terms of cybersecurity, some countries are more advanced than others. The United Kingdom is a leader, investing £1.9 billion to support cybersecurity development across three fields: (i) defending systems and infrastructure, (ii) deterring cybercrime/ cyber attackers, and (iii) developing a whole-society capability from the biggest companies to the individual citizen. Other countries with leading cybersecurity programs include the South Korea and Israel. Partnering with one of these countries could enable other countries to strengthen cybersecurity protection.

In support of a digital-driven recovery, we recommend strengthening consumer and small-business rights when contracting online, reinforcing data protection rules to include cloud infrastructure, and investing in cybersecurity prevention.

8) Ensure digital competition

Free and fair competition is necessary for the digital economy to thrive. Competition drives lower prices and higher-quality goods and services. Protectionism, whether to shelter national industries or incumbent providers, is a barrier to a smart economy.

Technology neutrality should apply to investment and regulation to ensure the best solutions are supported. Public procurement should encourage and reward innovation. At present, lack of flexibility in many public procurement systems is a major barrier to digital transformation. For example, many systems do not permit online document submission, e-signatures and paperless processes. Established ways of working and doing things are often protected by tradition and reinforced by tendering requirements. Effective competition must ensure digital solutions are fairly considered and can attract additional bidders.

Digital competition can also mean looking beyond national borders to support digital transformation. The United Arab Emirates (UAE), through its smart-nation innovation initiatives, has adopted and incubated the latest technologies. With limited R&D capabilities of its own, the UAE has invited competition from global players to provide digital infrastructure. It also attracts and supports a large ecosystem of start-ups to create value from its ICT infrastructure, encouraging overseas partnerships and collaboration.

We recommend that digital competition is boosted by reducing protectionism and encouraging collaboration to improve the quality and affordability of digital solutions.

The perfect policy mix for a rapid and sustained recovery

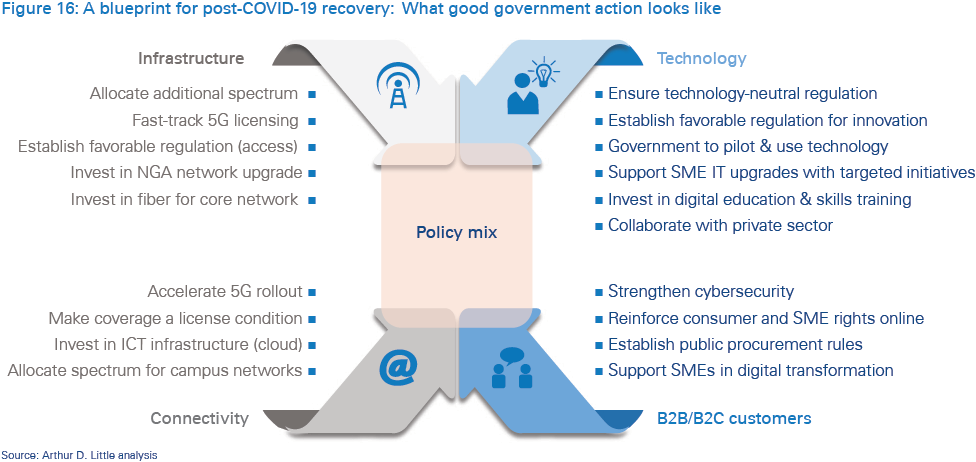

We have recommended an eight-point plan for governments to consider, positioning digital as a key enabler of the post- COVID-19 recovery. Bringing these recommendations together in what could be considered a best-practice policy mix, Figure 16 provides an action list under the headings of infrastructure, connectivity, technology and the B2B/B2C demand side.

While recognizing what stakeholders want from a digital transformation, we also believe that businesses should take action to support government efforts. Governments cannot do everything, and the most successful digitalization will involve government and business working together. Business-specific actions will, to a large extent, depend on the dynamics of the industry, including its digital capabilities, agility and current level of digitalization.

Conclusion

Digital solutions have had a profound impact during the COVID-19 crisis, enabling parts of the economy to continue to function online and through remote working. In other areas, digital solutions were needed to protect healthcare workers, and treat and care for patients. There now needs to be a consolidation of these digital advances across industries to establish the foundations for a deeper digital transformation and a strong and sustained economic recovery.

We consider the advances made during COVID-19 to be part of a longer-term trend towards a smart economy – characterized by autonomous systems, augmented processes, digitally represented assets, predictive systems and interconnected devices – that creates new business opportunities and productivity improvements.

Our research and client projects have convinced us that government action is needed to aid the post-COVID-19 recovery. Focusing on digital can accelerate the move to a smart economy and, in the process, accelerate economic growth for prolonged prosperity. Our eight-point plan for governments requires the following actions:

- Place digital at the core of the recovery strategy Investing in digital generates greater-than-average returns for the economy.

- Boost infrastructure investment The foundation of a smart digital economy is a strong and reliable infrastructure.

- Enable a digital recovery for all, not just the happy few Targeted initiatives supporting SMEs, the vulnerable and the disadvantaged are essential.

- Push “green” and digital together To multiply the benefits and ensure a sustainable recovery

- Double efforts to improve ICT skills and digital literacy Ensure that workers, companies and households have the capabilities to benefit from a digital economy.

- Use the government as a catalyst for digital adoption Tprovide digital leadership and pilot new technology.

- Empower small businesses and consumers Create confidence in the smart economy.

- Establish fair digital competition. Promote technology neutrality and encourage collaboration.

Overall, we believe that digital should be an engine for growth post-COVID-19, helping to prevent a protracted L-shaped recession and transform the economy. A smart economy promises improved productivity and new business opportunities over the longer term.

DOWNLOAD THE FULL REPORT

Putting digital at the heart of the economic recovery

COVID-19 has pushed digitalization everywhere. What’s needed now is the right government action to accelerate the transition to a smart economy.

DATE

Executive Summary

Digital technologies have played a crucial role in keeping society functioning during the COVID-19 pandemic, whether by enabling remote working, automating processes or facilitating contactless transactions. The increased use of digital technologies has also brought society closer to developing a smart economy, which promises new ways for businesses to grow and be more productive. We believe that governments need to accelerate these developments by placing digital at the core of the post-COVID-19 recovery, and propose an eight-point plan that sets out how digital technologies can be used to drive this recovery.

COVID-19: Part of a “perfect storm” bringing change

The past three decades have been characterized by rising global prosperity, with over 1 billion people lifting themselves out of extreme poverty, while a growing middle class has benefited from mass consumerism. Globalization and the internet revolution have created new business opportunities and improved productivity.

However, this positive trend has recently been upended by a perfect storm of threats to globalization, including rising economic uncertainty, increasing income inequality, and most recently, the COVID-19 pandemic.

COVID-19 in particular has rapidly impacted the way we live, do business, communicate with one another, learn and access information, feed ourselves, move around, and maintain our well-being.

Social distancing and other public-health measures introduced to combat the spread of COVID-19 have changed behaviors and brought scarcity of some goods and services. In several countries, entire populations have been under lockdown, with people required to stay home, shops and restaurants closed, public transportation suspended, and aircraft grounded. Our lives have continued, but much has changed.

Consumers and businesses alike have explored alternative ways of working and communicating, adopting new tools and methods they may not have considered before. Most notably, digital platforms have been used as a substitute for face-to-face interactions, often improving their efficiency.

As countries now begin to relax lockdown measures, the pace of recovery and adjustment to a “new normal” will differ by geography and industry. Different views of the future are emerging in the wake of COVID-19, including the technologies, business models and new behaviors it has introduced.

In this paper, we describe in Section 1 the impact and implications of COVID-19 for business; in Section II, we look at the role for digital in the new normal, identifying those industries that can benefit from digital transformation; and in Section III, we recommend what governments can do to encourage a sustained and rapid economic recovery.

1

COVID-19: Accelerating digital adoption and rethinking business models

The digital economy has benefited substantially from the COVID-19 crisis. Many of us now work remotely using cloud services and videoconferencing, consume entertainment from online subscription services (such as Netflix), order groceries and meals through digital platforms, and purchase a growing range of goods online. However, not all digital industries have benefited. Digital platforms that rely on human contact have suffered – for instance, ride hailing (e.g., Didi, Uber, Lyft) and property rental (e.g., Airbnb).

Figure 1 presents the impact of COVID-19 on the internet industry in Germany, based on research by Arthur D. Little for ECO, the German internet industry association. While there has been a pronounced shift in the share of B2B and B2C transactions carried out online, sales volumes declined as the economy shut down. A more nuanced analysis is therefore needed. Taking TV and video consumption as an example, Figure 1 shows that with many households in lockdown, consumption of TV has content increased. However, broadcasters have had to contend with plunging advertising revenues as the wider economy has contracted (not shown in the figure). Thus, the net impact on the industry may have been more negative than casual observation suggests. What COVID-19 has led to is a change in revenue share between traditional broadcasters and online streaming platforms. This move online to digital platforms has disrupted many sectors.

To better understand how COVID-19 is affecting different industry sectors, we have developed four categories of impact to evaluate the post-COVID-19 world:

- Rebound These are temporal changes which snap back to pre-crisis norms within relatively short periods. For example, apart from personal protective equipment being worn by employees, we would anticipate the demand for and provision of services such as hairdressing and taxi transport to change little post-COVID-19. Those familiar with the English pub might also expect crowds to return on match days to pre-COVID-19 levels. Equally, the availability of fresh foods at the grocer’s will likely return to normal as supply chains recover.

In a rebound, businesses seek short-term government support to survive until normal market conditions return. This support can include a deferral of business rates or tax relief. In the medium term, support is required to help businesses adapt to the new normal post-COVID-19. For example, investment in thermometry equipment to monitor and reassure both staff and customers, as these are safety measures that engender confidence, will support a rapid recovery. The “revenge consumption” seen in some countries as lockdown restrictions were lifted can be considered a severe rebound effect as consumer confidence returns.

- Substitution This refers to permanent or semi-permanent changes in behavior and demand for goods and services. The crisis has seen many households adopt digital solutions for the first time – even the elderly, who are typically more reluctant to try new technologies, have been encouraged by home delivery and contactless interactions. For others, the move online has accelerated, as digitally savvy consumers have expanded their use of online platforms to purchase a wider range of perishables, consumer durables and entertainment. In short, COVID-19 has accelerated the adoption curve for many digital solutions – demand shifts which are unlikely to reverse. (See Figure 2 for the UK.)

The evolution of delivery platforms in China provides some examples of how retail businesses have adapted and are now flourishing despite the disruption. Meituan-Dianping and Alibaba’s Ele.me dominate the delivery-platform market in China. Although use of these platforms was already widespread before the crisis, due to their focus on food delivery, several developments have since given a boost to revenues:

- Platforms have introduced innovations such as contactless deliveries and prepared meals for home cooking, improving customers’ choice if they want to cook fresh and healthy meals at home, which is attractive to younger demographics

- Platforms’ expansion into delivering books, cosmetics and smartphones, partnering with the likes of Huawei and Sephora – a beauty-products chain – has leveraged the network effects of these platforms.

- New customers, specifically older and typically less digitally savvy groups, have been attracted to the platforms.

Restaurants devastated by loss of walk-in customers during lockdown have also been encouraged to join these platforms to deliver restaurant food to homes, changing their business models in the process. Even Michelin-starred restaurants in London and Hong Kong have made the move to food delivery.

Consolidating the move online for many businesses means using online sales platforms to digitalize backoffice operations for greater efficiency. By gathering procurement and sales data in real time, businesses can monitor inventories more accurately, automate purchasing and improve business planning. New services can also be offered as business use of digital platforms evolves and deepens – store pick-up, same-day delivery, advanced loyalty schemes based on customer analytics, personalized marketing, etc. Faced with substitution, businesses need to realign their strategies and operations with the new normal to optimize benefits. This may mean revising business plans and strategies to accommodate accelerated digital adoption and changing customer behavior or target segments. For smaller businesses, support will be required to upgrade IT equipment and skills in order to benefit from the digital economy. Moving online is the first necessary step for businesses to recover and thrive in the new normal.

- Process This refers to changes in the ways of working and production incurred by COVID-19. New approaches have been developed during the crisis in response to social distancing and similar restrictions. Figure 3 illustrates how digital technologies have reinvented healthcare processes in response to COVID-19. The use of robots in hospitals to carry out repetitive tasks (such as cleaning and food delivery) has freed up valuable health-professional time for patient care. AI algorithms have enabled doctors to improve diagnosis reliability through augmentation. Manufacturing has been automated to protect workers. Drones have been used for last-mile delivery in logistics.

Digital tools enable businesses to redesign processes from the ground up, rebooting how work gets done and, in the process, redefining the business model to serve customers with improved products and greater efficiency. For example, in rail travel, this could mean automation of entire routes with driverless modules, which would allow capture of data at key junctures to manage passenger flows, provision of real-time journey information and insights to managers on asset condition and operational risks, and improvement of maintenance efficiency and reduction of downtime. Figure 4 provides a recent example of a rail operator using AI and machine learning to reinvent its risk management approach.

Home working is another process change that can be beneficial for employer and employee. A major telecoms player highlighted that its strong IT infrastructure had enabled its staff to work remotely and more flexibly during COVID-19 with no discernible impact on performance. Indeed, customers who normally had security concerns with different ways of working were much more accepting of new approaches and tools. A positive experience for both customer and supplier, experimentation has enabled this telecoms supplier to introduce more efficient processes.

With new technologies such as blockchain, the IoT and 5G communications currently being piloted in many industries and deployed at scale in others, we consider the current post-COVID-19 conditions conducive to further reinvention, rethinking of processes, investment and business planning.

- Revolution This defines cases in which both substitution and process changes occur in parallel. In other words, permanent or semi-permanent shifts in demand occur in tandem with process changes, which, in part, renders business models redundant. Industries are left to reinvent customer offerings and define more efficient processes and ways of working. Cruise tourism and passenger air travel are examples of sectors upended by the “perfect storm” of COVID-19 factors. In common with process changes, we foresee that these sectors will constantly evolve in the future to attract customers and improve operational efficiency. For example, augmented reality/virtual reality solutions will dispense with the need for many face-to-face interactions, leading to further reinvention.

Our prescription is to be bold. It is understandable that businesses may want to cut investment in a crisis and be more conservative in uncertain times, but bold decisions today can offer higher returns tomorrow. Moves such as rapid transformation from a restaurant to a delivery-based gourmet food-experience vendor, or migration of physical channels to online platforms (for banking and insurance processes), have saved businesses in the downturn and provided growth opportunities in the longer term. Bold businesses wishing to acquire new skills and digital capabilities through M&A will also find they can do so at lower cost in the downturn as valuations are depressed.

Due to the severity of disruption in “revolution” industries, government support is needed to make the bold yet necessary changes to create a sustainable future. For example, with airlines facing severe losses (see Figure 5 below), governments have provided cash injections to companies including Cathay Pacific, Lufthansa and Air France/KLM. The bold response is to use this cash to operate more fuel-efficient aircraft and reinvent service offerings around digital platforms, thus driving competitiveness, securing a sustainable future, and attracting customers back to air travel. Partnering with other stakeholders in the travel and transportation ecosystem is another bold initiative that could generate new efficiencies and create new service opportunities – for example, enhancing the door-to-door passenger experience.

Other challenges exist for airlines, such as protecting staff and passengers when onboarding and offboarding aircraft while maintaining social-distancing rules. Digital solutions to reduce human interaction can include app-based guidance and information for passengers, deployment of robots, and one-token travel identification. Predictive asset maintenance in operations and blockchain for the traceability of jet-engine parts in airline supply chains are further examples of where digital can reboot business models and help drive efficiency savings.

2

Digital in the new normal: Emergence of a smart economy

A smart digital economy

With rapid change and disruption continuing across many industries, the natural questions to ask are: where is this all leading? And how can businesses prepare and adapt for the future?

The changes we have described have a series of common features. They are:

- Autonomous through removing or limiting human interaction;

- Augmented to improve the effectiveness and efficiency of human actions;

- Highly agile and rapid in execution, and thus scalable;

- Digitally represented, enabling new insights to be gathered from data analytics;

- Interconnected and compatible, enabling devices to talk to and learn from each other.

These characteristics are consistent with what we consider to be a smart economy. The smart economy is enabled by multiple technologies with strong interdependencies. They include AI, machine learning, autonomous and assisted vehicles, edge computing, quantum computing, blockchain, big data analytics, and 5G telecommunications.

The end point in a smart economy is a fully connected and augmented world in which multiple devices talk and learn from each other to produce more efficient goods and services, which are personalized to the needs of the individual, with real-time functionality, and highly transactional. By being smart, industries improve productivity, create new opportunities for growth and generate higher returns. And by being able to pay higher wages, higher living standards and sustained economic prosperity are possible.

Indeed, for those economies and industries which have suffered weak productivity growth in recent years, a digital-led recovery from COVID-19 could be the step change needed to improve their long-term growth trajectory.

Digital as a driver of the economic recovery

As we emerge from the COVID-19 global downturn, a rapid recovery is needed to prevent a spiral into prolonged economic depression. A V-shaped recovery (Figure 6) is now looking less likely as the pandemic is still ongoing in many parts of the world, with exports remaining depressed and supply chains disrupted. As such, the focus is now on a U-shaped recovery.

While digital technologies offer new ways for businesses to grow and be more productive, it is not completely clear how investments in new technologies impact productivity. A World Economic Forum study attempted to shed light on this issue based on data from over 16,000 companies in 14 industries, which was subject to econometric analysis of the productivity impacts.

It made four key findings in relation to companies’ returns on digital investments:

- The return on investment in new technologies is positive overall. The productivity increase is three times higher when technologies are deployed in combination – as would happen in a smart economy.

- The return on digital investments varies by industry, and industry leaders achieve greater productivity increases from investments in new technology than followers do (70 versus 30 percent), which reinforces the view that digitalization is a continuous process and organizations need to be agile.

- Asset-heavy industries realize more value from robotics; asset-light industries realize greater value from mobile/ social media, primarily led by efficiency-driven opportunities.

- While industry leaders have realized higher overall returns from robotics and mobile/social investments, followers have gained more from the IoT and cognitive technologies (artificial intelligence and big data analytics).

Although more research is needed to fully understand the impacts of digital investment by individual industry and economy, the findings clearly support the assumption that digital investment generates more than average positive returns. With COVID-19 accelerating digital adoption and forcing the reinvention of processes and business models, we believe that building on these advances is the best course of action to kickstart growth and avoid a protracted L-shaped recovery.

What does smart look like?

To reflect on what is already ongoing in many industry sectors, here are some case studies showing what a “smart” world may look like. The selected cases demonstrate how digital can have a transformative impact.

Smart hospitals improve patient care and operational efficiency using autonomous, augmented and AI technologies

Aging demographics and rapidly rising costs are challenges facing public and private healthcare globally. The need to find new ways of working and efficiencies in healthcare delivery, while improving healthcare outcomes in treatment and prevention, are established priorities. Yongin hospital in South Korea was one of the first to introduce 5G, piloting several business use cases to improve patient comfort and generate operational efficiencies. (See Figure 7.)

We foresee healthcare being a leading beneficiary of digital technologies as the smart economy develops. Common features of future healthcare may include: telemedicine in pandemics to diagnose patients at safe distances, AI to aid doctors with diagnoses, patient monitoring via wearables, thermal imaging for body thermometry, chatbots for psychological consulting, and robots for logistics. The continual need to improve patient care and control healthcare costs makes it a fertile industry for the application of new digital technologies.

The airport of the future promises contactless, endto- end journeys and more efficient operations

Applying digital technologies to airports can transform the end-to-end journey for passengers and generate efficiencies for operators. Post-COVID-19, there is a need to attract passengers back to air travel and re-establish profitable operations. Many airports have plans to go digital, and some are already in the process of implementing 5G, robotics and other technologies to improve customer experience and operational efficiency. We foresee that this transformation will now accelerate, with innovative solutions needed for testing passengers prior to airport arrival, limiting human contact during key touchpoints (check-in, customs, border control, boarding, etc.) and automating ground-handling operations. Figure 8 illustrates some of the technologies that Etihad Airways and Geneva Airport have already implemented to create a smart airport. Other examples reported in recent months include one-token identification at Tokyo Narita Airport planned for the 2021 Olympics, facial recognition at Beijing Airport, and autonomous vehicles at Hong Kong Airport.

The airport of the future will look very different to airports of today. With 5G deployment on the horizon and business use cases emerging, we anticipate that airports and other transporthub operators will increasingly emerge as digital leaders.

Traceability, real-time tracking and contactless are features of smart logistics

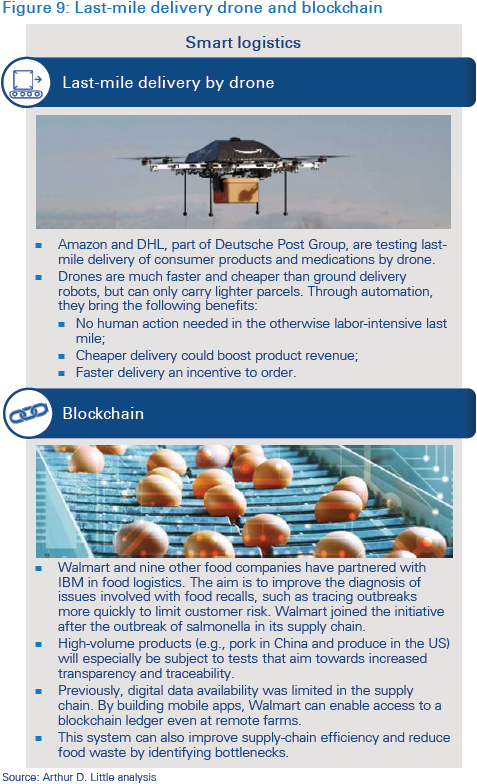

During COVID-19, a major challenge has been to introduce contactless last-mile delivery of medical goods and daily necessities to those with pre-existing medical conditions. Autonomous robots and drones were found to be an effective way of making these deliveries. A longer-term trend is the need to improve traceability and transparency in supply chains, for instance, to ensure the authenticity of pharmaceuticals or aircraft spare parts. For this, blockchain is being piloted to create immutable records in decentralized networks. Further examples of how these technologies are being used in logistics are provided in Figure 9, with more use cases certain to follow as supply chains become more complex and product origins need to be validated.

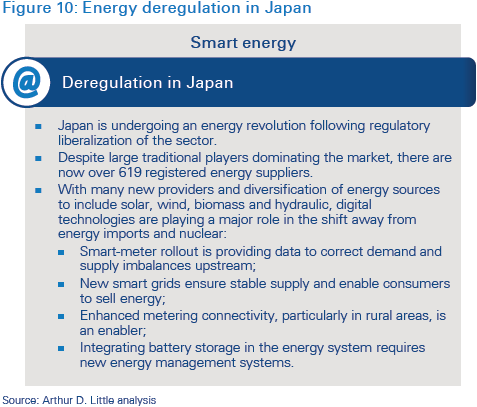

Smart energy grids are needed to connect new energy sources and safely manage energy supplies

Energy markets, specifically in Japan (as illustrated in Figure 10), some states in the US, and especially in Europe, are undergoing seismic changes that require digital solutions. To integrate renewable-energy sources with the power grid, manage supply and demand fluctuations, and enable the creation of the prosumer (households that sell surplus solar energy to energy suppliers on sunny days and consume energy on cloudy days), digital transformation is underway. Moving from centralized conventional generation technologies (coal, gas, nuclear) to decentralized renewable-energy sources (wind, solar, hydro) requires upgrading conventional grids to manage greater numbers of inputs and outputs, enabling real-time monitoring of energy consumption/production, and creating trading platforms for emission certificates.

We expect more regions to follow in the future, which will require 5G telecommunications, IoT devices, distributed ledger technologies and new business models to work in unison to manage energy suppliers and improve network resilience.

3 How to accelerate the economic recovery

We recommend an eight-point plan for governments to accelerate post-COVID-19 recovery via digital technologies:

1) Place digital at the core of the recovery strategy

Placing digital at the core of the recovery strategy and policy offers higher-than-average returns for the economy and society at large. This is why governments must include it in every single aspect of their recoveries, across initiatives and throughout all industries.

Aside from the economic benefits, going digital offers lifestyle and work changes that have positive impacts on the environment (fewer journeys and carbon emissions) and society (improved family life from working at home).

Fiscal stimulus packages with focus on digital include:

- South Korea A “Korean New Deal” aims to invigorate the convergence of new and old industries for greater job creation (see Figure 11), investing US$62 billion in establishing digital infrastructure, fostering industries that are online or do not require physical contact, and digitalizing infrastructure.

- European Union The European Commission is proposing to create a new recovery instrument: Next Generation EU – €750 billion of additional funding on top of an existing EU budget for 2021–2027 – a total of €1.85 trillion for a more sustainable, resilient and fairer Europe that places digital and green economic development at its core. (See “Push ‘green’ and digital together”, below.)

- Spain The central government is providing €16 billion to autonomous regions in support of two programmes: i) Giga society to encourage telecom operators to invest in better connectivity in low-yield areas; and ii) 5G pilot projects to fast-track deployment. The aim is to ensure all citizens and businesses (especially SMEs) can benefit from the digital economy.

The key levers for government are investment and regulation:

- Investment is needed to bring forward 5G deployment and next-generation access networks (NGA networks), and support business investment in digital transformation initiatives (training, ICT infrastructure, technology pilots, etc.). Investment is also required in digital cloud infrastructure (data centers), accompanied by regulation to determine where data is to be stored and computed, and under which regulatory framework

- Regulation should be used in parallel with investment. For example, placing obligations on telco operators (e.g., to connect rural/low-yield areas) and/or setting targets (e.g., for electric-vehicle deployment) can be powerful incentives for business and enablers of transformation.

More favorable regulation can also encourage private sector investment. Favorable regulation includes improved right-of-way access for infrastructure development, and rules that permit different business models and technologies to be applied in each market. Technology neutrality is critical if the best solutions are to be developed and find commercial value. In highly regulated sectors such as financial services and utilities, regulators should permit new products and business models, provided the risks created are adequately managed. Regulatory sandboxes are increasingly used to test new technologies in a controlled environment where the risks of a new business model or product can be assessed and understood. An example is the blockchain strategy of Germany’s federal government. Working with the tech industry, the regulator (BaFin) is defining the legal framework and supporting investment in this disruptive technology. As a result, Germany is becoming a blockchain leader.

2) Boost infrastructure investment

One of the core roles for governments is to provide infrastructure for its people and industries. This is even more critical for the digital economy: digital and ICT infrastructure must be a priority for governmental investment during the recovery, to lay the foundations of the smart economy. We would encourage public investment to go hand-in-hand with private investment in this area through public-private partnerships (PPPs).

High-quality fixed broadband should penetrate over 99 percent of households and businesses. Fiber and 5G rollout should be accelerated to give all businesses and households access to online opportunities in the digital economy. Regulators should also be encouraged to increase the spectrum available for 5G and LTE services, which can include short-term licenses or local licenses for campus/private networks. IT infrastructure investment is also required, particularly to enable SMEs to fully partake in the smart economy.

Many countries have now allocated 5G spectrum to operators, typically through auctions. However, to speed up the deployment of 5G, we recommend allocating more spectrum for unlicensed/shared usage. Large industrial sites, airports, sports stadiums and conference venues can make use of this additional spectrum to test and pilot new applications more quickly rather than wait for the widespread deployment of 5G. For example, we see smart-city initiatives in Hong Kong, Vienna, and Seoul deploying 5G in designated areas to accelerate use-case piloting and monetize the benefits.

Recognizing that 5G will help drive economic recovery and encourage business investment, New Zealand scrapped a planned 5G spectrum auction during COVID-19, implementing instead a fixed-price tariff to accelerate introduction. Japan adopted a similar policy, allocating 5G spectrum for free to operators, with obligations to invest in network development and coverage in exchange for licenses. The major benefit of these approaches is that operators have more capital left in the bank for infrastructure rollout. The opposite occurred in Italy, with auctions raising huge revenues for regulators, but leaving little on the balance sheets for deployment, which may now be delayed.

Arcep, the French regulator, has adopted a similar approach to Japan, requiring 25 percent of 3.4–3.8 GHz band sites in 5G deployment to be located in sparsely populated areas, thereby stimulating economic activity, notably manufacturing, and achieving high penetration and universal access, not just in metropolitan areas. Despite resistance among some operators and potential delays to 5G spectrum auctions, investment obligations are a better way of supporting a digital-driven recovery than via record-setting auctions.

3) Enable digital recovery for all, not just the happy few

The benefits of digitalization should be available to all. Inclusive access recognizes connectivity as a human right and an essential component in building a smart economy

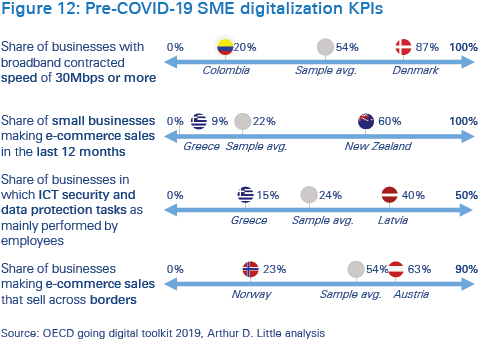

A large digitalization gap exists between the world’s “haves” and “have nots”. For example, ADL research on SMEs (Figure 12) found that 87 percent of SMEs in Denmark had access to broadband speeds of at least 30 Mbps. In Columbia, this figure was 20 percent, and the sample average was 54 percent. The connectivity gap was equally wide between many urban and rural communities, with frequent media stories of homeworkers forced to walk up hills or visit coffee shops to access the connectivity necessary for videoconferencing or similar digital platforms.

For SMEs, targeted government initiatives are needed to boost access for all businesses. Figure 13 identifies a number of targeted initiatives to support SMEs, including the provision of information to allow small businesses to make informed decisions, investment to enable digitalization, and ready-made solutions that businesses can adopt and/or participate in to boost revenues.

Access goes beyond SMEs and connectivity to also ensure that individuals have the necessary IT equipment and software. In some cases, this requires assistance for those who are most vulnerable in society. Recognizing that digital inequality is a major issue, the European Commission has introduced a digital inclusion policy supported by four initiatives to close the gap (Figure 14).

4) Double efforts to improve ICT skills and digital literacy

The effectiveness of digital investments in driving the economic recovery will depend to some extent on how businesses and individuals make use of digital solutions. Strong ICT skills and digital literacy are needed to optimize their use.

For some, this may involve learning how to use a tablet or online platform for the first time. For others, updating existing skills and developing new capabilities can create value and opportunity. For the more digitally savvy, upskilling more workers in programming and advanced technologies is needed to ensure businesses can recruit from a larger pool of capable workers. Indeed, a focus of South Korea’s New Deal is the training of new AI and software talents.

Among schoolchildren, measures implemented during COVID-19, such as free software licenses (Hong Kong) and laptops (UK), have been effective in boosting the number of students able to participate in lessons online and develop e-skills. For adults, Microsoft has offered six-month free subscriptions to its Teams software, which, in part, has accelerated the move to remote working for individuals and businesses.

In summary, a digital recovery for all should continue the initiatives introduced during COVID-19 to connect all households and businesses, as well as improve IT equipment access and skills.

5) Push “green” and digital together

As society becomes more environmentally conscious and aware of the need to address climate change, going digital should also mean going “green”. Virtual working and more efficient production go hand in hand with a cleaner environment and reduced resource depletion.

In launching the EU’s proposal for its next-generation stimulus package, European Commission president Ursula von der Leyen explicitly tied green outcomes to the recovery and digitalization, stating:

“The recovery plan turns the immense challenge we face into an opportunity, not only by supporting the recovery but also by investing in our future: the European Green Deal and digitalization will boost jobs and growth, the resilience of our societies and the health of our environment...”

The proposal provides additional stimulus funding via taxes on non-recycled plastics and carbon emissions, among other revenue sources. South Korea and Germany have also included environmental objectives in their post-COVID-19 stimulus plans. As these are export-led economies aiming to be leaders in electric vehicles, green energy infrastructure and autonomous technologies, a dual digital/green policy focus is a logical step to support industry competitiveness.

It is not just export economies that can benefit. For instance, Pakistan has also introduced a green COVID-19 stimulus package to improve energy efficiency and resilience in its construction sector.

6) Use the government as a catalyst for digital adoption

To drive broader digital transformation of the economy and reward innovation and reinvention, governments must do two things:

Firstly, government should embrace digital technologies to improve the quality and efficiency of public services. Denmark is a leader in this regard. (See Figure 15.) By becoming a digital leader itself, government demonstrates confidence in the technology, positively signalling its benefits, reliability and affordability to businesses and households. Early support can accelerate private sector adoption and encourage further innovation by establishing a market for innovators.

Secondly, government should leverage its position as a user and regulator of digital services to establish standards and remove regulatory obstacles to digital adoption. For example, asset tokenization and smart contracts based on blockchain technology are slow to penetrate markets. Establishing regulatory frameworks that provide legal certainty, develop standards for how data is managed, and specify minimum performance requirements can accelerate adoption and development.

Our recommendation is that governments should be bold, not just in investing in digital. Governments should use digital solutions and create the regulatory conditions conducive to innovation.

7) Empower small businesses and consumers

Empowering consumers and small businesses to adopt and use digital technologies is an important factor in accelerating the economic recovery. Consumers and businesses must have confidence in the reliability and security of digital solutions, but also have the information to hand to make informed purchasing and data-sharing decisions. A recent example is the reluctance of many to use COVID-19 tracing apps in some countries over concern for data security and privacy. Similar concerns exist for small businesses when sharing data in industry consortia or with suppliers.

Publishing use cases is an important first step in understanding the benefits of a technology and what additional risks it may generate. From a legal perspective, consumers want reassurance that a digital purchase is equivalent to making a physical purchase (i.e., the level of protection and rights are the same whether a download or physical product).

Measures are ongoing to strengthen security and protection for small businesses and consumers in the digital economy, with due consideration given to maintaining digital sovereignty. The European Union’s digital single market is one of the most prominent examples, and it is currently in the process of implementing laws to protect businesses and consumers online, which include:

- New rules to stop unjustified geo-blocking;

- Strengthening consumer rights when purchasing online and cross-border;